On Demand (Part I)

Section V.2A and V.2B of II.1 ("The Problem of Scale (Part I)"): Considering "The General Theory" of Lord Keynes

V.2A

…Cadell Last’s work on “Metasystem Transition Theory” in my opinion strongly speaks to a dialectic between creativity and energy as foundational to human civilization and its evolution. ‘Both energy and information as phenomena appear to fundamentally influence human system structure and also appear to build on previously establish processes,’ Cadell writes, ‘allowing higher controls to stabilize new organization and complexity.’ For more on HMST theory, please see his work in The Global Brain Singularity. Similarly, speaking with Robert Breedlove, Michael Saylor made the point that money is an energy system, and wherever there are inefficient monetary systems, a social order suffers for it. Saylor notes that we cannot cheat gravity, energy, or physics: what happens is what happens in science, and there is no cheating. For Saylor, money today invites and enables cheating, and as a result the monetary system is dysfunctional. In his view, replacing the fiat system with bitcoin would help solve this problem, and furthermore help the information and “energy” systems which money makes possible to be more efficient and productive. Unlike gravity, money can be an imperfect system, and stopping that requires us to make a point to do better. For Mr. Saylor, the more money is like gravity, the more it will be like a universal language, communicating similar outputs to the population, and more people will hold a shared understanding of the financial system. In this way, the financial energy of society will be better structured, and if indeed value ultimately results from creativity and energy, then a more efficient “social energy” will translate into a more efficient society.

I very much like the idea of “money as energy system,” which helps align it with “the dialectic between creativity and energy.” Indeed, it does seem like money is “a socially constructed energy system,” that though useless on a desert island, is still in the high majority of (social) situations extremely important. In fact, the “island thought experiment” presented in this paper may only help provide reason for us to think that we should consider money “like energy,” for if energy is paramount on a desert island, and money is so critical in most social settings, then perhaps money is “a social energy” of some kind. In this way, I believe the thesis of this paper suggests the correctness of Mr. Saylor. Furthermore, the notion of “money as an energy system” might help us transition into Keynes and understand why the constant flow of liquidity is central for an economy, without which demand cannot be stimulated or realized. However, though socially I believe demand mostly manifests in and through “the energy system of money,” it is not the case that demand fundamentally is money and its movement. Liquidity is easily the social manifestation of that deeper fundamental reality, and by studying society we then might glimpse those fundamentals.

After Lord Keynes, “demand” is arguably the most central concept in all economics. Before The General Theory, it was believed that markets operated according to an “equilibrium” that basically “worked itself out”: if prices were too high, people would stop buying and bring prices down to prices they could afford; if unemployment increased, it must mean that either people didn’t want to work, didn’t need to work, or employers weren’t offering inadequate wages; if goods were bought in large quantities, it must mean the goods were valuable and in high demand — and so on. “Market equilibrium” basically means that “zero-sum events” are impossible: everything ultimately proves either to be “balanced out” or “non-zero-sum,” meaning either ultimately everyone benefits or everything evens out. This is basically the “efficient market hypothesis,” and it meant government intervention or involvement was unnecessary and even detrimental. “Total collapse” was impossible in the Classical Model (except because of always unnecessary intervention), for a fall of wages here was made up by a fall of prices there, a loss of jobs here was made up by new employment opportunities over there, and so on. And Keynes did not dispute that this kind of “self-correction” happened in Capitalism, but he did argue that it didn’t necessarily happen. This is critical: what Keynes is arguing is that the success of Capitalism isn’t determined (“deterministic” or even “scientific,” as perhaps defined the zeitgeist of his age). “Freeing” the market won’t necessarily liberate the market to ascend; it could, but we could also be releasing the market to fall and crash.

To make an overarching point against all “self-correcting market equilibria,” Keynes focused on employment and more particularity the possibility of “involuntary unemployment,” which is what we will focus on here. ‘The traditional theory maintain[ed], in short, that the wage bargains between the entrepreneurs and the workers determine[d] the real wage,’ Keynes wrote, which meant that wages resulted from negotiations, and if wages were low, it basically must have been the case that negotiations collapsed for some reason.²⁹⁸ ²⁹⁹ ‘If this [was] not true,’ Keynes added, ‘then there [was] no longer any reason to expect a tendency toward equality between the real wage and the marginal disutility of labour.’³⁰⁰ To speak very generally, following the “Classical Model,” “involuntary unemployment” was an impossibility, for if someone wanted a job, it had to be available somewhere. But witnessing the Great Depression between 1929 and 1939, it seemed ridiculous to Keynes that this could be explained simply by claiming that people wanted to be unemployed and/or that people were unwilling to work for wages being offered to them. Something deeper and more systemic had to be at work, and the target of Lord Keynes was a theory of Capitalism that suggested it necessarily returned to a state of equilibrium. Keynes arguably never proved Capitalism wouldn’t ultimately self-correct, and he himself acknowledged that, but he did prove that the downturns could be far longer than any of us imagined. And in the long run — to allude to a line from Keynes that even children know — we’re all dead.

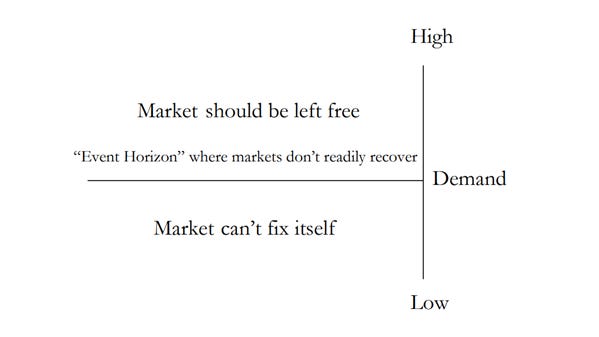

‘The ultimate object of our analysis,’ Keynes wrote, ‘is to discover what determines the volume of employment.’³⁰¹ As Derrida discussed finding a small detail in a philosophical system that tugging on could bring the whole system down and/or open up new possibilities, so Keynes “tugged” on the assumption that “involuntary unemployment” was impossible and deconstructed “market equilibrium” as practically reliable. No, to stress the point, Keynes did not show that market would never return to equilibrium, nor did he show that “the logic of equilibrium” or “free market Capitalism” never applied or worked. Mainly, Keynes showed that “free markets worked” contingently, and basically only if “demand” in the economy didn’t dry up. If demand was strong, “free markets” worked, but if demand vanished, free markets couldn’t repair themselves (in a timely fashion, and perhaps never). If demand was strong, markets should indeed be left alone and free, but Keynes would have the State always be ready to generate and offer demand in the economy, because if demand fell below a certain level, the market would collapse and, in its freedom, do nothing but roll and wallow in squalor. The following chart might help explain:

Demand is central for Keynes, and it is not the case that freedom necessarily maintains demand. In freedom, we are free to commit suicide, and likewise we are free to dry up demand. If this occurs and the market drops below a certain “Demand Event Horizon” (DEH) that is very difficult to pinpoint ahead of time (which is a major problem), then the market slips into a downward spiral which it cannot recover from back to normal/high levels of demand.³⁰² Since the free market working is contingent upon demand being present (at a certain amount), if this “event horizon” is crossed, the free market will easily be like Humpy Dumpty: broken and unable to put itself back together again. The king and his men will need to help. Before Humpy Dumpty falls, he’s free to do what he wants on the wall, but once he falls, he can do little. Again, this doesn’t mean a market below DEB can’t ever recover (that’s unknown), but that it likely takes an incredibly long-time, during which the people might rise up against the government, the cities might crumble apar — and it takes far longer to build something than tear it down.

As we fall below the DEH, it becomes like the scenes in the movie Interstellar where time changes on the water planet. The crew investigates the plant while leaving a crewmember on the spaceship, and when the crew returns, twenty years have passed, and it turns out the crewmember was left on the ship by himself for two decades. As the crew approached the water planet, time sped up for them while slowing down for everyone else. Similarly, the more we fall below the DEH, it is like we approach the water plant, and the amount of time it takes for the market to recover “on its own” begins to multiply rapidly. If we fall just slightly below the DEH, we might be alright, but the nature of a DEH is to “keep pulling us lower” once we cross it, so it will be difficult for us to only fall “slightly below the DEH” without “the pull of gravity” taking us much lower. And the more we fall, the longer it will take for us to “recover” — if we ever escape at all. Once we fly into the “pull” of a blackhole, our chances of escape are slim; similarly, once the force of a DEH begins to pull on us, our chances of not falling into a very elongated Depression are also low. For Keynes, at all costs, we must avoid this fate, but how?

The fact the exact point this “event horizon” cannot be pinpointed is a problem, because it means we can find ourselves nervous about crossing this line without meaning to, and that means every crisis the State might jump in and create demand (even if it shouldn’t, but who can say? The fact we can’t might benefit Discourse). If it is perhaps true that “free markets are best” and that State action tends to create inequality (for example), then the default action of the State could be to always “jump in” to avoid the Apocalypse, meaning we might end up in a “suboptimal state.” But what else should we do? Sit around and do nothing? Well, for me (as will be explained), the probability that State action isn’t needed to maintain demand is relative to the size of the Artifex class (a term coined in “The Creative Concord” by O.G. Rose), which is basically just “the creative class” (of entrepreneurs, artists, etc.), but that is contingent to how much creativity is present in the system. If creativity is low, government intervention is likely needed, which means we must take a great risk, at which point no strategy seems clearly best. Personally, I would prefer to just maintain a strong Artifex, but that might be too late for us now (unless Discourse has not yet prevailed).

If demand is indeed the necessary precondition for free markets, then what is demand? What’s fascinating to me is that once we cease to believe that markets “take care of themselves,” we suddenly must become much more philosophical, because it becomes clear that we create demand and that thus demand must somehow reflect us. Demand ceases to be this mysterious “spirit” out there which makes sure the market returns to equilibrium under all circumstances, a “hand of Providence” which assures us that “fully employment” will always be with us, and instead demand is contingent. What is “noncontingent” is arguably “infinite,” something not to be toyed with by mere mortals, but what is “contingent” is “finite,” and thus is a product of finitude and finite being. Keynes seems to be like Nietzsche, declared “Equilibrium is dead!” and now we find ourselves having to “make ourselves worthy of the murder.”³⁰³ Before Nietzsche, we could believe our morals, values, and social structures were “given to us by God” (saving us existential anxiety), and, since God was good, there was reason to think they would “take care of themselves” as long as we were Christian (at least in the West). Christian societies “self-regulated” (in a Christian worldview), while Non-Christian societies fell apart, so all we had to do was “stay Christian.” Likewise, if we believe Capitalism “self-regulates,” all we have to do is “stay Capitalist,” and the rest will take care of itself. But as Nietzsche gives us a revelation that “reaches back in time” and changes the meaning of all history (a “flip moment”), so the thought of Keynes changes the meaning of Capitalism throughout all time, not just moving. Capitalism is suddenly contingent, a thing we make work or fail, as suddenly became the case for Christianity. We as Christians suddenly could fail, and so it now goes with Capitalism. Yes, there is still an “invisible hand,” for there are still emergent systems and results, but no longer can we assume that this “invisible hand” generates “the best of all possible worlds.” The devil could just as easily be “the lord of this age” — the complexity of Paul’s vision of sovereignty and providence can no longer be glossed over.

What do we demand? Why do we demand it? Who are we to demand this and not that? All the existential questions come rushing in once demand ceases to be disembodied and “out there”: we suddenly must own our values (and, forcing us to accept this, perhaps it’s no wonder that Keynes can be rejected–nobody likes fighting their ego). But it would seem to me that facing existential questions is necessary for people to be Artifexian: philosophy and creativity are deeply related (as hopefully “The Creative Concord” by O.G. Rose made clear). When it came to “the death of God,” the madman asked, “Is not the greatness of this deed too great for us?” We can ask a similar question with “the death of equilibrium,” and I think by the shrinking of the Artifex, we have reason to say that the answer is currently “yes.” Fortunately, I don’t think it’s too late for us to change our answer, especially once we learn of Rhetoric and its primacy against Discourse.

V.2B

Keynes wants to know how poverty can be possible ‘in the midst of plenty.’³⁰⁴ Critically, counter to the Classical Model, he concluded that ‘the mere existence of an insufficiency of effective demand may, and often will, bring the increase of employment to a standstill before a level of full employment has been reached.’³⁰⁵ If this is the case, then “market equilibrium” is false, and why exactly is because ‘the struggle about money-wages primarily affects the distribution of the aggregate real wage between different labor-groups, and not its average amount per unity of employment, which depends, as we shall see, on a different set of forces […] The general level of real wages depends on other forces of the economic system.’³⁰⁶ And now we can see why Keynes called his work “The General Theory”: he wants to argue that though there can be isolated and particular examples of “returns to equilibrium,” this is not will occur generally if demand collapses. Generally, the collapse of demand marks the end of the possibility of “equilibrium,” and it’s even possible that if demand collapses in x sector, it will spread over to y sector where “equilibrium works,” and then suddenly y will no longer function “on its own.” Collapses in demand can spread, so it’s critical that the State acts quickly to reconstitute demand before the “event horizon” noted above is crossed (the fear of which could cause the State to “overreact” and unnecessarily risk inflation, the Austrian may note).

‘[T]he contention that the unemployment which characterizes a depression is due to a refusal by labour to accept a reduction of money-wages is not clearly supported by the facts,’ Keynes asserted strongly, for though there might be isolated instances where unemployment is due to this, it cannot generally explain the whole Great Depression.³⁰⁷ Considering the great suffering, it was unimaginable to Keynes that it was all self-inflicted, that the misery he witnessed was what people wanted or were willing to suffer as they waited for another job to come along that offered higher wages. It had to be the case that jobs simply weren’t available, Keynes concluded, which means unemployment was most involuntary, which basically meant Classical Models had to be incomplete, for Classical Economics contended that ‘unemployment, which [was] […] involuntary, [couldn’t] occur.’³⁰⁸ Why was this assumed? Well, to again put the case generally, ‘supply [supposedly] create[d] its own demand,’ and that means if there was (even just possible) supply, there would be a need for workers to realize and distribute that supply, because the very existence of that supply would assure a demand for it.³⁰⁹ Since basically there was always “some kind of supply,” there would always be a need for workers, and the rest took care of itself. Yes, I understand the case is more complex than this, but I think the main ideas are present well enough and outlines the main structure against which we need to ‘work out the behaviour of a system in which involuntary unemployment in the strict sense is [actually] possible.’³¹⁰ For involuntary unemployment was present during the Great Depression, and that mean the economy we believe followed a Classical Model actually followed something else.

According to the Classical Model, supply was central, for supply would create its own demand, which would then create employment opportunities. When prices fell, supply would be cheaper, and people would jump upon these “cheap prices” with their savings, which would create demand and employment, restoring the market to equilibrium. Since the market was at equilibrium at some point, there had to be savings somewhere in the system, and Classical thought held a deep ‘notion that if people [did] not spend their money in one way they [would] spend it in another.’³¹¹ In other words, if people didn’t spend their money before the market downturn, they would spend it during the downturn, for the only reason they wouldn’t have spent it is basically because they were wise and waited for better prices. Not spending savings during a downturn would be irrational and foolish, and since the market was rational, people would take advantage of “the sale,” assuming there were savings available, and the Classical Model was basically setup to conclude there always would be savings. And, please note, Keynes had a lot of respect for Classic Economics and did not deny that this was “the way the market worked” above the “event horizon” described above in the graphic. But if that “event horizon” was crossed, savings would be dried up.

Why would savings not be available if the market fell below “the event horizon?” Well, if demand dried up, business would dry up, and that meant wages would dry up too. If people weren’t making wages, they wouldn’t have money to spend on businesses, and so businesses would fail. Without businesses, people wouldn’t have income, and so new businesses wouldn’t recover, and critically savings will have dried up on the way down. People must eat, after all, and as the market gradually collapsed, wages would fall faster that necessary consumption, and when the bottom “reached bottom,” there would be no savings left to take advantage of the cheap prices. Worse yet, if anyone still had money left, it would likely be the rich and upper classes, so the downfall would easily just increase inequality. Austrian and Classical Economists argued that thrifty entrepreneurs finally receive an opening during a market downturn, that downturns are some of the rare opportunities when the rich can finally be dethroned and class movement realized. But though Keynes wouldn’t deny some of that could occur, the majority of “savers” aren’t entrepreneurial, and the few entrepreneurs out there who could take advantage of “the sale” will lose all their savings on the way down, either because they buy too early and lose value as the market falls further (eventually going bankrupt), or because they would run out of money while they waited for the market to settle down. For Keynes, it was far more likely that a DHE would be passed and/or that only the rich would benefit from the downturn.³¹²

In my view, a key line which sums up Keynesianism is found in Chapter 6 of The General Theory, centered in the middle of the page:

‘Income = value of output = consumption +investment

‘Saving = income — consumption

Therefore saving = investment.’³¹³

This is critical. For Keynes, savings that aren’t “in” investments are “practically” of no economic relevance at all. If I have a $1000 in the bank, it has no relevant to the macroeconomic picture, but if I have $1000 invested in oil, my $1000 is relevant and productive. Yes, I have $1000 in both cases, but they are not the same regarding their role in creating demand and production, and they especially aren’t if we accept Keynes believe that people who save $1000 in the bank are psychologically and emotionally unlikely to ever invest it (especially in a downturn that scares them), as will be expounded on later. Couple this belief with the idea that the $1000 in the bank will gradually dwindle to $500, $100, and then $0 as the market falls, meaning no money will be left to “buy up the cheap prices,” and the $1000 invested in oil is radically more valuable than the $1000 in the bank (especially if maintaining demand is everything, as Keynes argues: the $1000 “not in the fight” is like a soldier who goes AWOL). Worse yet, Keynes believes the $1000 invested will entail a “multiplier effect,” which means the invested $1000 will work out to, in macroeconomic terms, be “worth” way more than a $1000, while the $1000 in the bank isn’t so multiplied. The two are simply incomparable. Yes, the invested $1000 could be lost, but for ever $1000 lost that it’s invested, there will be a $1000 that triples it’s worth, while the $1000 in the bank will be safer but much more useless. In the long run then, “investment” turns out to be the only “real” savings that matter.

If savings are investments, then savings which aren’t investments don’t exist. This point should be stressed: savings for Keynes which weren’t investments were, for all practical purposes, nothing at all. Spending was real, but savings were nothing but potential, and unrealized potential was nothingness. Since Keynes believed the very personalities of savers meant they would likely fail to realize the “potential” of their savings well, and also since Keynes thought they wouldn’t invest during downturns because the savings would dry up, the “macroeconomic relevance” of savings should have been assumed to be zero. The only “real” savings were investments, and so it became critical for Keynes that savers weren’t supported in their emotional dispositions and habits by high interest rates. This might sound strange, for we spend our lives being told that “spenders” are the ones who need to learn morals and restraint, but Keynes here is introducing us to the possibility of “vice savers,” those who save out of fear, trepidation, and a lack of discernment to know what to invest in. We will expand more on this later, but it should be noted that Keynes has support in his thinking in the work of Adam Smith (surprisingly enough).

Concerning the General Theory ‘the propensity to consume will, in what follows, take the place of the propensity or disposition to save.’³¹⁴ It might be going too far, but Keynes basically wants us to disregard savings from our economic considerations. ‘The decisions to consume and the decisions to invest between them determine incomes’ — notice what Keynes doesn’t say, mainly that “savings” have anything to do with incomes.³¹⁵ Savings are irrelevant (pure potential), and, in the wrong hands, even harmful, which suggesting why it is so problematic that Classical Economics lionizes and praises savers. Yes, savers who will become investors are wise, but saving isn’t a virtue for its own sake, an impression easily made by Classical Economics. If savings dried up demand and caused us to fall below the DEH, savings would actually be a vice.

If “savings are investment,” then whatever makes investment possible is also what makes savings possible, and for Keynes that is “demand.” Here though we have a “chicken and egg problem”: Do people demand something after an investment, or does investment created demand? This question will be returned to on the topic of “the Artifex,” but here establishing the necessity of demand for investment (in whatever order) is enough to proceed with the argument. All we must grant is that low interest rates stimulate investment, which is a well-established macroeconomic reality (though perhaps wrong). Recall though that Classical Economics would have us raise interest rates during a downturn precisely to incentive savings, so that — it was supposed — people would have the money to afford the supply (which inherently ‘creat[ed] its own demand’).³¹⁶ But if Keynes is right that “savings are investment,” then a policy which slows investment also destroys savings. ‘For aggregate saving is government by aggregate investment; a rise in the rate of interest […] will diminish investment.’³¹⁷ Ultimately, because of the interconnectedness of the economy, ‘when the rate of interest rises, the rate of consumption will decrease,’ and that means ‘saving and spending will both decrease.’³¹⁸ Bringing his argument together, Keynes wrote:

‘The rise in the rate of interest might induce us to save more, if our incomes were unchanged. But if the higher rates of interest retards investment, our incomes will not, and cannot, be unchanged. They must necessarily fall, until the declining capacity to save has sufficiently offset the stimulus to save given by the higher rate of interest.’³¹⁹

It would be hard to emphasis how staggering this claim was at the time it was stated, and it basically is the knife of “Nietzsche’s madman” still dripping with the blood of “market equilibrium” (below DEH). Keynes sums his position up with well-place italics: ‘to save more out of a given income […] will decrease the actual aggregate of savings.’³²⁰ “Out of” is the key phrase, for Keynes is suggesting that savings outside of investment is money that we can no longer call “income” — it’s basically lost.

Classically, as has already been argued, “supplies was demand,” and the market assured everyone had income to realize their demand. ‘The classical theory assume[d], in other words, that the aggregate demand price (or proceeds) always accommodate[d] itself to the aggregate supply price.’³²¹ Following Say’s law, this meant ‘that the aggregate demand price of output as a whole [was] equal to its aggregate supply price for all volumes of output, [which was] equivalent to the proposition that there [was] no obstacle to full employment.’³²² In other words, markets self-corrected. Well, Keynes argued this position assumed demand would always be there, and Keynes was adamant this was not “given.”

Generally, for Keynes, the problem was that Classical Economics divided “supplies” from “savings,” whereas in Keynes we could say that “investment” is “supple/savings,” per se. Keynes wanted us to “save in supply,” not separate savings from supply, whereas Classical thought wanted supply to flow through the economy while savings sat on the side, waiting for opportunities (in the hands of “virtuous savers”). Keynes seems to much prefer the term “investment” to “supply,” and frankly it seems a way to understand Keynesianism is to remove “supply” from our lexicon. In Keynes, “investment” should be our focus, for that naturally generates “supply” secondarily, without us having to focus on it. Following C.S. Lewis, if we put things first, we get second things also, but if we put second things first, we lose both. Investment leads to supply, but emphasizing supply could lead to investment drying up, causing us to lose both. Why? Well, again, it’s basically because people will hold money on the side waiting for investment opportunities, and there, on the side, the money will go to waste.

Keynes wants us to cease dividing “supply” from “savings,” for that sets us up to think we should save up waiting for an investment opportunity, when it is precisely because we are saving our money that this investment opportunity may never manifest, because demand in the economy will dry due to the lack of investment. Do you see the logic here? “Supply” and “savings” either rise together or fall together, so Keynes wants us to think of them as “one and the same” in hopes of making us think clearly about both. Where they are divided in our minds, various ethics and morals can “creep in” that contribute to saving instead of investing, and Keynes wants to make it very clear that there is nothing ethical about saving money unless it’s ultimately “in” investment, considering all the harm “pure savings” (what could be called “savings outside investment”) can cause in drying up demand and contributing to a horrifying and devastating fall below DEH. This doesn’t mean we should never save money, for we indeed need money to invest, but it does mean that we can’t just save money. Keynes wants us to make “saving/supply” the foundation of our “economic ethics,” not just savings, and he calls that “investment.” Investors, who are savers and (wise) spenders, are greater moral heroes than “pure savers.”

Classical Economists viewed savings “left on the perimeter” of the economy, divided from supplies, and the assumption was that savings would come “racing in” when the market failed to “save the day,” picking demand and supply back up. As a result, new entrepreneurs would be born, the thrifty would be rewarded, and the positions of the upper class would change hands. Savings were “the fail safe,” and since wise people saved (according to CEs, as I’ll now call them), the wise would handle “the failsafe” and be rewarded for doing so; then, “market equilibrium” would be reestablished. But Keynes claimed this was not the case: Capitalism proved not to be so virtuous on its own. It wasn’t the case that enough savings waited on the sidelines to stop the economy from falling below DEH, and even if it did, many of the savers were actually “vice savers” (as will be expanded on) who would do nothing but sit on their savings as the economy failed. Hence, CE would fail to save the day, and the consequences would be incredibly dire.

We can view the critique of Keynes against CE as two-sided. First, he doesn’t want us to assume that “supplies” was necessarily the same as “investment” (though the categories could overlap), for the language of “supplies” contributes to thinking of savings as “outside” market activities (though Keynes of course spoke of “supplies”), ready to race in like the calvary before the market collapsed. Instead, Keynes wants to emphasize “investment,” which places savings “in” the economy. The only savings are “savings in” investments; for Keynes, everything else is just that: “everything else.” The sooner “savings” can be turned into “savings in,” the better, and however the State can stimulate that transformation, it should. But Hayek and others worried about potential inefficiencies this could cause: when people felt pressured to invest, they tended to invest poorly, and this could contribute to “bubbles.” But Keynes didn’t worry about “bubbles,” for he believed even Pyramids were better than nothing, but that must be explained later regarding “the multiplier.” If Keynes had to err, he preferred being frivolous than inactive, not that he supported frivolity.

Second, Keynes didn’t believe “demand was given” (“our god could die,’ per se). CE assumed that “demand would always be with us,” but Keynes saw this assumption as dangerous. It was possible for there to be all the supplies in the world and not the slightest bit of demand for it, because it was possible for a people to lack any wages to realize their wants and desires. People simply didn’t have money when the economy collapsed to “take advantage of all the deals and opportunities,” and/or the amount of savings available was such a radically small fraction of all the money needed to “bounce back” the economy that it wouldn’t make a difference. Savings couldn’t be relied on to restore demand, and worse yet the people with savings would probably prove too scared to take any risks during “a downturn.” Thus, demand could dry up in Keynes, and that meant the State had to be ready to supply demand when needed, or otherwise the market would fall below the DEH and stay there for years, decades, centuries, and perhaps longer. And for no reason, Keynes thought, because there was no virtue in risking and surviving a Great Depression. Rather, the virtue was found in stopping it, but realizing this required that we killed another virtue system first. That was the assumed “virtue of the saver,” an idea that need problematizing with “the vice saver”…

.

.

.

Notes

²⁹⁸Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 11.

²⁹⁹The blame was usually put on the shoulders of workers for being unwilling to work for less pay, suggesting they were lazy, which could entail negative psychological impacts.

³⁰⁰Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 11.

³⁰¹Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 89.

³⁰²This brings to mind “Trading Wages for Hours” by O.G. Rose, where it is argued that the Federal Reserve faces a similar problem of an “indeterminable point.”

³⁰³Allusion to “The Parable of the Madman” by Nietzsche.

³⁰⁴Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 30.

³⁰⁵Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 30–31.

³⁰⁶Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 14.

³⁰⁷Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 9.

³⁰⁸Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 16.

³⁰⁹Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 18.

³¹⁰Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 17.

³¹¹Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 20.

³¹²But doesn’t Keynesianism contribute to inequality? Indeed, that is an argument often made, for Keynesianism is often used to increase asset value and investments, and more often than not it is the rich who hold assets and investments. This could suggest that “upper classes” solidify their power with forms of “deterrence,” as discussed throughout O.G. Rose. Perhaps “deterrence” is the defining feature of Capitalism today, though I’m not sure.

³¹³Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 63.

³¹⁴Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 65.

³¹⁵Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 64.

³¹⁶Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 18.

³¹⁷Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 110.

³¹⁸Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 111.

³¹⁹Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 111.

³²⁰Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 111.

³²¹Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 26.

³²²Keynes, John Maynard. The General Theory of Employment, Interest, and Money. Orlando, FL: First Harvest/Harcourt, Inc., 1964: 26.

.

.

.

For more, please visit O.G. Rose.com. Also, please subscribe to our YouTube channel and follow us on Instagram, Anchor, and Facebook.